Maximum 35-year mortgage more than enough

Bank Negara Malaysia (BNM) said a maximum loan tenure of 35 years is “more than sufficient” for borrowers to settle their housing loan by their retirement age.

It said increasing the loan tenure will further add to the cost of financing without significant improvements in the affordability of the borrowers’ monthly instalments.

In July 2013, the central bank capped the maximum loan tenure at 35 years for the purchase of residential and non-residential properties as part of its responsible financing measures.

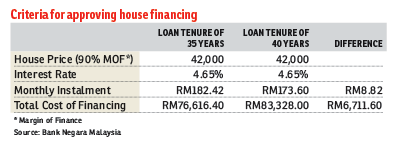

In a statement yesterday, BNM said for a new borrower who takes a loan of RM42,000 for 35 years at 4.65% per year and can get 90% margin of financing, the equated monthly instalment (EMI) will be RM182.42. If the loan tenure is extended to 40 years, the EMI would be RM173.60. This means an additional cost of RM8.82 per month.

The total cost of financing for 35 years, meanwhile, stands at RM76,616.40. Choosing a longer tenure loan of 40 years will result in an additional cost of RM6,711.60 to a total cost of financing of RM83,328.

Recognising that the overall economic slowdown may impact housing affordability, BNM said it has been engaging the various state authorities in the issue of financing for affordable homes. The government is forecasting the Malaysian economy to grow between 4% and 4.5% this year, down from an earlier forecast of between 4% and 5%.

“The central bank, together with the state governments and the banking industry, is working to align the criteria used in approving house financing and improving the affordability of the applicants,” BNM said.

The central bank also said it is important for borrowers to disclose accurate material information about their financial position, including their credit history, when applying for house financing to ensure objective assessment by financial institutions.

“The assessment by banks on borrowers is partly to assist [the latter] in ensuring that they have the capacity to service the loan throughout its tenure. The assessment takes into account the applicant’s income after statutory deductions, expenditure on necessities and all debt obligations from banks and non-bank lenders.

“This is to ensure that borrowers can continue to service their obligations, have sufficient financial buffers for living expenses, and are able to protect themselves against rising costs and unexpected adverse events, including the foreclosure of homes,” it added.

BNM also advised borrowers to compare housing loan packages offered by various financial institutions for the best price. “Some banks have introduced housing loan products such as first home schemes for specific target markets, including young married couples, youths and low-income groups.”

The central bank also pointed to the Credit Counselling and Debt Management Agency, which it said has been providing advice to applicants to rationalise their debt levels and educate them on prudent financial management.

For those who do not have the capacity to own a house, BNM said they may consider the option to rent.

Source: TheEdgeProperty.com.my

This is a stupid example.

Take a RM500,000 – RM1,000,000 and calculate

Then you feel the difference